What Is Term Life Insurance?

Term life insurance is a type of life insurance that provides coverage for a specific period of time, such as 10, 20or30 years. If you pass away during that term, the policy pays a death benefit to your beneficiaries.

This type of coverage is designed to offer affordable financial protection during your key earning years. Many people use term life insurance to replace income, help pay off a mortgage, or cover major family expenses if they die unexpectedly.

How Term Life Insurance Works

Term life insurance works by providing coverage for a defined period of time in exchange for regular premium payments. As long as premiums are paid and the policy remains active, the coverage stays in force for the full term.

The policy is structured to deliver predictable financial protection during years when your family may depend on your income or financial support.

Where Your Premiums May Go

Your premiums are primarily used to cover the cost of providing life insurance protection during the policy term.

A portion of each payment supports underwriting, administrative, and operational expenses for the insurer. Because term life insurance does not build cash value, premiums are not directed toward savings or investment accounts, which helps keep costs lower than permanent policies.

What Happens If You Die During The Term?

As long as the policy is active and premiums are paid on time, coverage remains in force throughout the term.

If you die during the coverage period, the insurer pays the full death benefit to your designated beneficiaries, provided the cause of death is not excluded by the policy. The benefit is typically paid as a lump sum and can be used for income replacement, debt repayment, or everyday living expenses.

Once a claim is filed and required documentation is reviewed, the payout is generally issued within a short processing period.

What Happens If You Outlive The Term?

If you outlive your term life insurance policy, coverage usually ends and no death benefit is paid.

Many policies include a renewal option, which allows you to continue coverage after the term expires. Renewed coverage typically comes with higher premiums because rates are based on your age at renewal, not when the policy was first issued.

Some policies also offer a conversion option, which allows you to convert your term policy into permanent life insurance without a medical exam.

What Term Life Insurance Covers

Term life insurance is designed to pay a death benefit if the insured person dies while the policy is active. In most cases, coverage applies to a wide range of causes of death, but specific exclusions and policy conditions can affect whether a claim is paid.

Understanding what is typically covered and what may be excluded helps set clear expectations before you buy a policy.

What Term Life Insurance Usually Covers

Most term life insurance policies provide coverage for the following situations:

Death from natural causes, including illnesses such as cancer, heart disease, stroke, or complications from chronic health conditions.

Death caused by accidents, such as car accidents, workplace incidents, or other unexpected events, as long as no policy exclusion applies.

Death occurring at any point during the active policy term, provided the policy is in force and premiums are paid as required.

Financial protection for beneficiaries, who can use the death benefit for income replacement, mortgage payoff, childcare costs, education expenses, or other household financial needs.

What Term Life Insurance May Not Cover

Certain situations may limit or prevent a payout under a term life insurance policy, including:

Death during the contestability period if the insurer discovers material misrepresentation or omitted information on the application.

Suicide within the initial policy period, as defined by the policy contract, which may result in limited or no payout.

Death after a policy has lapsed due to unpaid premiums beyond the grace period.

Specific policy exclusions, which may include certain high-risk activities or occupations, depending on the insurer and underwriting terms.

Key Features of a Term Life Insurance Policy

A term life insurance policy includes a set of core features that determine how coverage works, how long it lasts, and how flexible it is over time. Understanding these features can help you choose a policy that fits your financial goals and budget.

Coverage Amount and Term Length Options

Most people choose a coverage amount that helps replace income, pay off major debts, or support children through important milestones like college.

Term lengths commonly range from 10 to 40 years, though some insurers offer longer options, such as 35- or 40-year terms. The right combination depends on your age, budget, and how long your loved ones would need financial protection.

Related term length guides:

10-year term life insurance15-year term life insurance20-year term life insurance25-year term life insurance30-year term life insurance

Free Riders:

Accelerated Benefits Rider: Lets you access part of your benefit if you're diagnosed with a qualifying illness or condition.Including:

Accelerated Benefits Rider for Terminal Illness (ABR)

Accelerated Benefits Rider for Chronic Illness (ABR)

Accelerated Benefits Rider for Critical Illness (ABR)

Accelerated Benefits Rider for Critical Injury (ABR)

Accelerated Benefits Rider for Alzheimer's Disease (ABR)

Lifetime Income Benefit Rider: The Company agrees to provide the option to elect a guaranteed lifetime income subject to the terms and conditions of this rider. After the conditions to exercise this rider are met, the Owner is guaranteed a lifetime benefit payment in exchange for a charge taken from the Accumulated Value of the policy to which this rider is attached.

Charitable Matching Gift Death Benefit Rider (CMG):provides up to $10,000 of the base face amount will be matched by insurance company if a charitable beneficiary is named.

Conversion Options

Many term life insurance policies include a conversion option that allows you to switch to permanent life insurance without any medical exam. This feature can be valuable if your health changes or if you later decide you want lifelong coverage.

Read: Converting Term Life to Whole Life

Renewal Options

If your term coverage is ending and you still need protection, renewal allows you to extend the policy without reapplying. Premiums increase because renewal pricing is based on your age at the time of renewal.

Renewal is often used as a short-term solution, especially if you’re not ready to replace or convert your coverage.

Types of Term Life Insurance

Term life insurance isn’t one single product. While all term policies provide coverage for a defined period of time, they differ in how premiums are structured, how underwriting works, and what type of financial need they’re designed to protect.

Understanding the main types can help you choose a policy that aligns with your financial goals.

Level Term Life Insurance

Level term life insurance provides a fixed death benefit and level premiums for the entire term, such as 10, 20, 30 or 40 years. This is the most common type of term life insurance and is widely used for income replacement, mortgage protection, and long-term family expenses.

Key characteristics of level term life insurance:

Premiums remain level for the entire term.

Death benefit does not change over time.

Often requires full underwriting, which may include a medical exam and records review.

Simplified Issue Term Life Insurance

Simplified issue term life offers level term coverage but uses a streamlined underwriting process. Instead of requiring a full medical exam, approval is based on health disclosures and data-driven evaluation, such as:

Answers to structured health questions

Prescription history checks

Height and weight build guidelines

Tobacco use

Motor vehicle records

Criminal history disclosures (where applicable)

Since underwriting relies on defined criteria and electronic records rather than lab testing, decisions are often faster. However, eligibility criteria for this policy type may be more rigid compared to fully underwritten policies.

Premiums are typically based on age at issue, and while they may remain level during the selected term, costs generally increase significantly if the policy is renewed at a later age after the initial term expires.

Simplified issue term policies can seem appealing to individuals who want longer-term level coverage without involving traditional underwriting or medical exams.

Decreasing Term Life Insurance

Decreasing term life insurance features a death benefit that gradually declines over time, while premiums typically remain level. It’s often used to cover specific debts that shrink over time, such as a mortgage or business loan, rather than ongoing income needs.

Return of Premium (ROP) Term Life Insurance

Return of premium term life insurance refunds the premiums you paid if you outlive the policy term. These policies cost more than standard level term policies and are best suited for people who want term coverage with the potential to recover their premium payments.

Annual Renewable Term (ART) Life Insurance

Annual renewable term life insurance provides coverage for one year at a time and renews annually without a new medical exam. Premiums increase each year as you age, making this option most appropriate for short-term or temporary coverage needs.

How Much Term Life Insurance Do You Need?

The right amount of term life insurance depends on how much financial support your dependents would need if your income were no longer available. Instead of focusing on income alone, consider the full picture of current obligations and future expenses.

Key factors to include:

Income replacement: Estimate how many years your household would rely on your income and multiply that by your annual earnings.

Outstanding debts: Include large obligations such as a mortgage, car loans, credit cards, or business debt.

Future expenses: Account for planned costs like childcare, education, or college tuition.

Existing assets and coverage: Subtract savings, investments, and any life insurance you already have, including employer-provided coverage.

Simple Rule Of Thumb

A common guideline is to choose term life insurance coverage equal to 10 times your annual income. This amount often provides enough protection to replace income, pay off major debts, and cover everyday living expenses for several years.

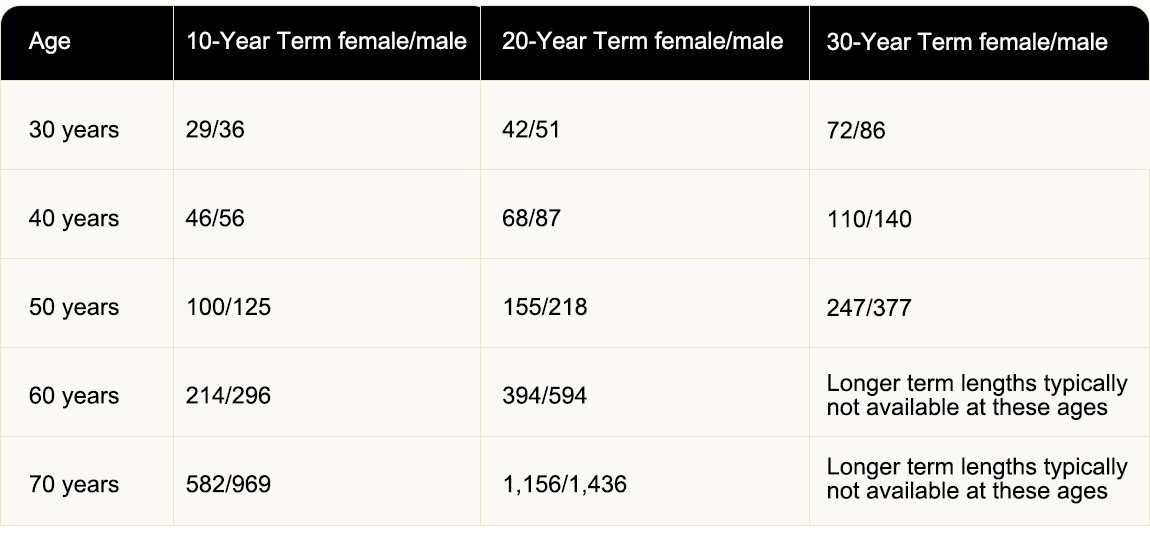

How Much Does Term Life Insurance Cost?

Term life insurance is typically one of the most affordable types of life insurance, especially for younger applicants or those in good health. Monthly premiums depend on factors such as your age, health profile, coverage amount, and the length of the term you choose.

In general, healthy adults can often secure a $1,000,000 term life insurance policy for tens of dollars per month, while costs increase with age, longer term lengths, and higher risk profiles.

Below are sample monthly premiums based on a healthy individual seeking a $1,000,000 term life insurance policy across different ages and term lengths.

Factors That Impact the Cost of Term Life Insurance

Life insurance companies determine term life insurance rates by assessing risk during underwriting. Several personal, lifestyle, and policy-related factors influence how much you pay in monthly premiums, including:

Age at application: Younger applicants typically qualify for lower rates, since insurers associate age with lower mortality risk.

Overall health and medical history: Conditions such as high blood pressure, diabetes, or prior serious illness can increase premiums.

Lifestyle habits: Tobacco use, heavy alcohol consumption, or participation in high-risk activities may result in higher rates.

Coverage amount: Policies with higher death benefits cost more each month.

Term length: Longer terms, such as 40-year policies, generally cost more than shorter-term options.

Underwriting class: Insurers assign a health classification during underwriting, which plays a major role in pricing.

Family medical history: A family history of certain conditions may affect long-term risk evaluation.

How to Get Affordable Term Life Insurance Rates

While some pricing factors are outside your control, there are practical steps you can take to lower your term life insurance premiums or improve your chances of qualifying for better rates:

Apply as early as possible: Locking in coverage at a younger age can secure lower premiums for the entire policy term.

Choose coverage based on actual needs: Selecting the right coverage amount and term length helps avoid paying for unnecessary insurance.

Improve your health before applying: Managing weight, blood pressure, and cholesterol may help you qualify for more favorable underwriting classes.

Avoid tobacco use: Non-smokers typically pay significantly lower life insurance premiums than smokers.

Compare term life insurance quotes: Rates can vary widely between insurers for similar coverage, making comparison essential.

Consider no-exam policies when appropriate: Some applicants may find competitive pricing and faster approvals through no medical exam options.

Pros and Cons of Term Life Insurance

Term life insurance offers affordable, straightforward coverage for a specific period of time, making it a popular choice for income replacement and major financial obligations. However, because coverage is temporary and does not build cash value, it may not be suitable for long-term or lifelong insurance needs.

Understanding the advantages and disadvantages of term life insurance can help you decide whether it aligns with your financial goals, budget, and coverage timeline.

Pros of Term Life Insurance

Affordable premiums for high coverage amounts, especially compared to permanent life insurance

Simple policy structure typically with level premiums during the term

Flexible term lengths, typically ranging from 10 to 30 years

Effective for income replacement, mortgage protection, and major family expenses

Faster application process, with many policies offering quick approvals

Cons of Term Life Insurance

Coverage ends when the term expires unless you renew or convert the policy

Premiums increase significantly upon renewal, since rates are based on your current age

No cash value or savings component, unlike permanent life insurance

Not designed for lifelong coverage or estate planning needs

May be harder to qualify for new coverage if your health changes later in life

Term Life Insurance vs Whole Life Insurance

Term life insurance and whole life insurance both provide a death benefit to your beneficiaries, but they are designed for very different financial needs. Term life insurance offers temporary, affordable coverage for a specific number of years, while whole life insurance provides permanent coverage and includes a cash value component.

The right choice depends on how long you need coverage, whether you want lifelong protection, and how much you’re willing to pay in premiums.

Key Differences Between Term Life and Whole Life Insurance

Feature

| Term Life Insurance

| Whole Life Insurance

|

Coverage Duration

| Covers you for a set period, such as 10, 20, 30 or 40 years

| Provides lifelong coverage as long as premiums are paid

|

Premiums

| Typically much lower and may remain level during the term

| Higher premiums that remain level for life

|

Cash Value

| Does not build cash value

| Builds cash value over time that can be accessed through loans or withdrawals

|

Flexibility

| Choose term length and coverage amount based on temporary needs

| Designed for long-term stability and lifelong planning

|

Policy Loans

| Not available, since there is no cash value

| Available once sufficient cash value has accumulated (loans reduce the death benefit if unpaid)

|

Best For

| Income replacement, mortgage protection, and covering high-expense years

| Lifelong coverage, estate planning, and guaranteed protection

|

Is Term Life Insurance Worth It?

Term life insurance is worth it for people who need affordable coverage to protect against temporary financial risk. Whether it makes sense depends on your dependents, debts, and how long your income would be needed if you were no longer there.

In general, term life insurance is best for covering temporary financial needs, while permanent life insurance is better suited for lifelong or estate-planning goals.

Term Life Insurance May Be Worth It If

You have dependents who rely on your income for everyday living expenses.

You are paying off major financial obligations, such as a mortgage, student loans, or other long-term debt.

You want a higher amount of life insurance coverage at a relatively affordable monthly cost.

You only need coverage for a specific period, such as until children are grown, debts are paid off, or retirement savings are established.

Term Life Insurance May Not Be the Best Fit If

You want lifelong life insurance coverage that does not expire.

You are looking for a policy that builds cash value or supports long-term wealth accumulation.

You expect to need life insurance well into later adulthood without renewing coverage.

Your primary goal is estate planning, legacy creation, or passing wealth to heirs.